Are you facing the daunting prospect of foreclosure? You’re not alone. In this no-nonsense guide, we’ll walk you through everything you need to know about foreclosure and pre-foreclosure, empowering you with the knowledge to make informed decisions and potentially save your home.

Pre-foreclosure is the initial step of the foreclosure process and generally starts when a homeowner falls behind on his or her mortgage payments. This becomes the most critical time frame in which ways are still possible for a homeowner to take action prior to actually going into full foreclosure.

The steps below explain how the process generally occurs and how to resolve it.

– It begins after several missed payments

– Lenders issue a Notice of Default

– Homeowners still have options to resolve the situation

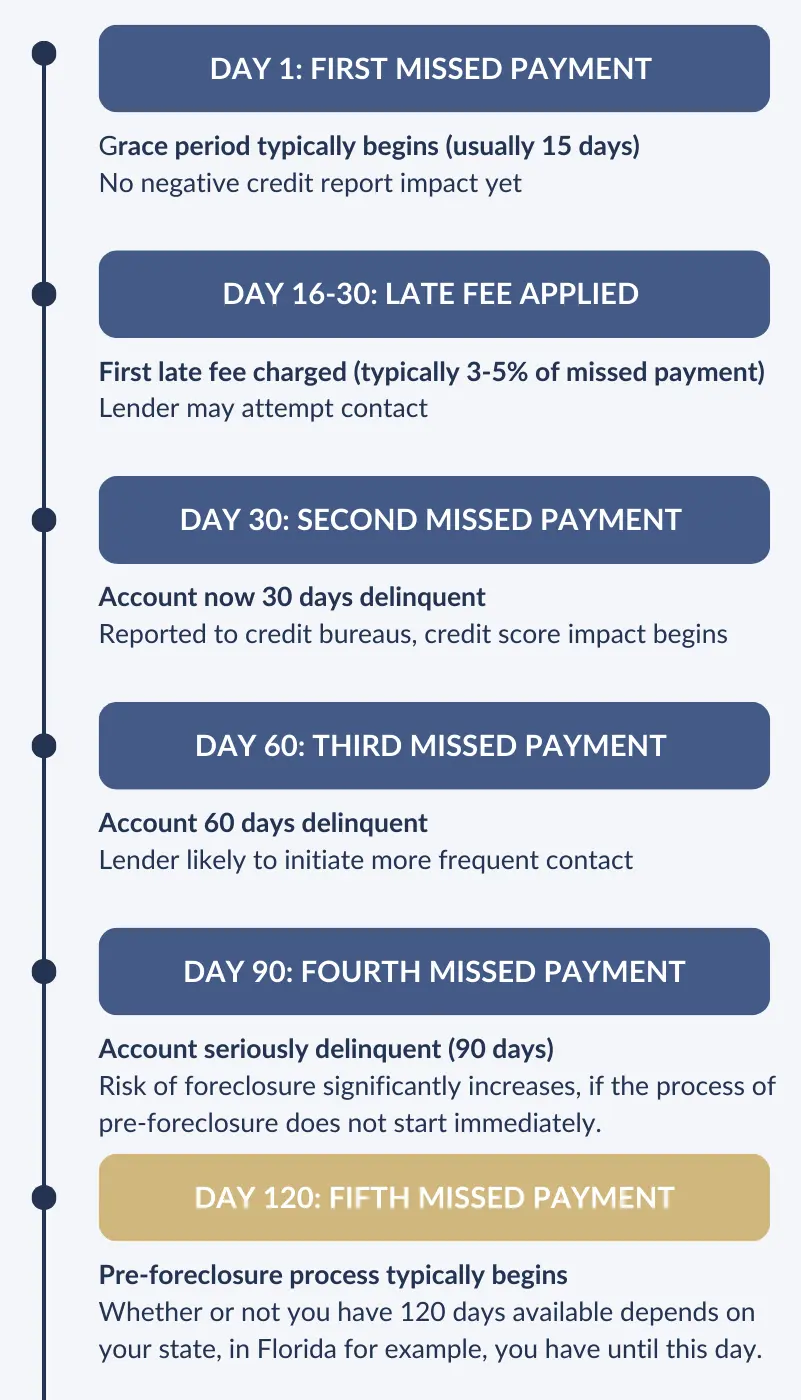

This is a general timeline of how the process goes:

The exact number of missed payments that will trigger foreclosure will vary, but generally, the lender starts the process after 3-6 months of missed payments. Generally, the timeline would be like this:

1st missed payment: Grace period initiated

2nd missed payment: Assessment of late fees

3rd missed payment: At an increased risk of foreclosure

4th missed payment: Possibly begins the process of foreclosure

Above all, never stop communicating with your lender. Many lenders offer forbearance options or payment plans to get you caught up.

If you DO miss all payment options then at some point between the days 150 to 180, a Notice of Default will be issued, marking the official start of the foreclosure process.

This becomes public record, that means they are publicly available, even online in multiple sources, the main one being your county’s office page, where you must search for the NOD (Notice of Default).

Other pages like Zillow, Foreclosure Real Estate Agents, Bank websites, or even newspapers also hold this information.

A NOD is a key document in the process of foreclosure because it is the lender’s formal declaration that the borrower is delinquent in payments on the mortgage and has fallen behind. It is a formal filing that can be construed as the actual beginning point—indeed, sometimes the real turning point—for homeowners.

The process the lender follows starts by recording the NOD with the county recorder’s office, after which the homeowner is served the document via certified mail. In some states, it may also be posted on the property.

At this point, it now has become a public record, possibly damaging the homeowner’s credit score, and the reinstatement period begins, usually lasting 90 days, and allowing the person to catch up and stop the foreclosure.

However, the NOD in many cases activates the acceleration clause on your mortgage, meaning that the entire loan balance is made due in full immediately.

The document generally includes:

I want to make it very clear then that at this point, It’s a warning sign that requires immediate action, but you still have options to save your home.

When facing foreclosure, many homeowners wonder if they will receive any money. The truth is, most homeowners won’t realize any money from having to sale in this situation.

Why?

Remember, for the lender, at this point the main priority in any foreclosure sale remains to recover the outstanding mortgage balance with its fees.

The proceeds will be tipically distributed in the following order:

First Mortgage: The primary lender gets paid first.

Additional Liens: Any junior lienholders (e.g., second mortgages, tax liens) are paid in order of priority.

Foreclosure Costs: Expenses related to the foreclosure process are covered.

Homeowner: Lastly, if any money remains after the above are paid, it goes to the former homeowner.

However, some exceptions might exist depending on your case, for example:

1. Surplus Funds: This happens in the case where the sale price exceeds the total debt and costs, so you are entitled to the excess.

Example: Your home sells for $300,000, but you only owe $250,000, including all fees and liens. You should be able to get $50,000 back.

2. Right of Redemption: Some states allow a “right of redemption” period after foreclosure.

During that time, usually 30 days to 2 years, you can get back your property by paying the full amount owed.

If you can’t redeem the property but the sale price is more than what you owed, you may be entitled to the difference as explained before.

3. Junior Lien Payoffs: If you had more than one mortgage or more than one type of lien on your property, any remaining balance AFTER the first mortgage is paid will go to junior lienholders.

Although you do not get this amount, such payment reduces the net debt that was to be accounted for.

This is the reason why most of the time with foreclosure sales, you just break even and pay off the mortgage and all the fees you owe.

When facing an imminent foreclosure auction, time is of the essence, so I organized 7 Key Ways you can use to Halt the auction process immediately.

Filing for bankruptcy is the most powerful weapon to stop a foreclosure auction instantly.

Automatic Stay: Upon filing, what is issued is an “automatic stay”, which literally stays or stops every collection activities, thus that includes foreclosure.

You have two options here, Chapter 13 vs. Chapter 7:

In Chapter 13, you may remain in your house and cover your payments in 3-5 years.

Chapter 7 may have the ability to merely put off foreclosure temporarily but prevent in some specific instances.

The bad side to this is that Bankruptcy stays on your credit report for 7-10 years and can have a damaging effect on your ability to get a loan in the future.

Please, take this as surface information, always talk to a bankruptcy attorney before declaring.

It’s possible to make a loan modification deal with your lender that will prevent a foreclosure auction from taking place.

Some ways in which you can get them to modify the loan, can be an easing of the interest rate percentage, a loan term extension, or maybe even a partial forebearance or forgiveness of the real estate property principal.

So you can manage this you can turn in a completed application with income and expense documentation and a hardship letter.

If the temporary forbearance is accepted, the creditors will halt the foreclosure process while the loan modification proposal is in consideration.

Also, look for options like the Flex Modification program for Fannie Mae and Freddie Mac loans.

This is what happens, should you make payment of the full amount that is due, together with all the missed payments, late fees, and foreclosure costs, so that foreclosure is stopped immediately. For this there are 2 main options:

Afterwards, make sure to obtain written verification from the lender that your account has been reinstated.

Here you sign over to your lender the ownership of your deed as a consideration to cancel your mortgage.

This includes a negotiation process, due to the fact that it has to be approved by both parties; lenders are not bound to take one.

Try to have the lender waive a Deficiency Judgment.

This process still does credit harm, however, it is less severe than that of foreclosure. As for the tax implications of the matter, canceled debt MAY be reported as income.

Perhaps the thing everyone thinks of when one says one is facing potential foreclosure: a short sale. So, up front, let’s do a side-by-side comparison of the two:

| Factor | Short Sale | Foreclosure |

|---|---|---|

|

Credit Score Hit |

50 – 130 points |

200 – 400 points |

|

Duration on Credit Report |

7 years |

7 to 10 years |

|

Future Home Purchase |

After 2 – 3 years |

After 5 – 7 years |

|

Control over Process |

Some control |

Little to no control |

|

Emotional Impact |

Difficult but less stigma |

Frequently more stressful and stigmatizing |

To put it simply, this is the option to sell your house for less than the balance of your mortgage WITH lender approval to avoid a foreclosure auction.

Though a short sale may be preferred under many circumstances, the Lender Approval IS required for all short sales and it is a very long and exhausting process.

You would need to work with a Real Estate Agent experienced in short sales to determine the best option for your situation.

And there is a documentation process where you must build a package with financial statements, hardship letter, and proof of income for a short sale.

The earlier you start this process, the better. It can take several months.

Try to negotiate with the lender to waive their right to come after you for the difference between sale price and loan balance.

In some cases, foreclosure may be stopped by taking legal action, a court order can stop a foreclosure auction.

For this you would have to sue the lender for wrongful foreclosure, if the lender is not acting properly.

This way, if the case is valid, state court issues a Temporary Restraining Order (TRO) and may halt or prevent the ongoing process.

Some states provide for a statutory right of redemption, whereby a borrower can recover after the foreclosure sale of their property.

It ranges from 30 days to as long as two years, depending on the state. In Florida, for example, this time is of at least two years, supposing you could cover the total foreclosure sale price, plus expenses.

Not all states have this; consult your state laws.

Regardless of what you choose, remember, the most important part is to ACT QUICKLY.

Many of these options are much less viable if you are close to the auction date. Keep a detailed record of your contacts with your lender, and Understand the Consequences; Each option has different effects on your credit and financial future.

While these methods can stop a foreclosure auction in its tracks, the majority of them are rather complicated and inappropriate for most people.

For those who may need a quicker, easier solution, there is another option worth looking into: selling one’s house for cash.

When you are facing foreclosure, time may be of the essence. Though effective in their own right, the techniques I have discussed can also be prolonged and involved.

Many homeowners seeking to avoid the headache and hassle of foreclosure altogether and who desire a speedy resolution will find selling their home for cash to be an attractive alternative.

The Advantages:

Selling for cash is a way out for any house owner who is about to lose his or her house due to foreclosure. Cash home buyers majorly buy homes in any state and sell them after doing all kinds of repairs, and do all the legalities required for the transaction, hence saving the house owner from complex legal procedures.

Through the cash home buying process, sellers make sure to sell their homes quickly, enabling them to proceed with their lives and thus avoid the adverse repercussions of foreclosure.

Provide us with your contact information by filling out our form.

We’ll reach out to schedule your appointment, at which your offer will be presented.

Pick your closing date, and get your cash!

Provide us with your contact information by filling out our form.

We’ll reach out to schedule your appointment, at which your offer will be presented.

Pick your closing date, and get your cash!

Our goal is to arrive at a solution that works best for you under your own unique circumstances and yields maximum benefit to you and your family.

If you are open to finding a solution by selling your home for cash in order to avoid foreclosure, we’ll be more than glad to be of assistance. Our professional cash home buyers will walk you through every process and give you a no-obligation cash offer for your property, ensuring that the transaction is as smooth as possible and hassle-free.

Contact us today for information on how to avoid foreclosure with confidence.

Your home is more than a financial asset; it is the fundamental ingredient in your life.

Equipped with this information, I hope that you will at least be better prepared to face the challenges of foreclosure and make decisions most conducive to your future. With the right approach and acting quickly, you may be able to save your home or at least minimize the long-term effects of foreclosure.